Blog

Subscribe to our NEWSLETTER to receive news, updates, and valuable tips.

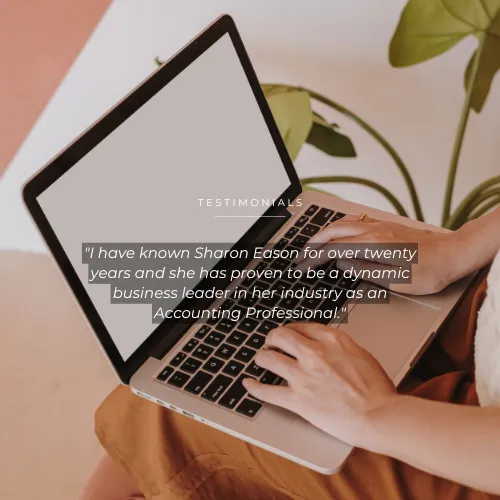

Qualified Small Business Stock (QSBS): How Business Owners Can Protect Seven-Figure Gains

How Business Owners Can Protect Seven-Figure Gains

There are very few places in the tax code where Congress openly rewards risk-taking.

Qualified Small Business Stock (QSBS) is one of them.

Yet even among successful business owners and early investors, QSBS is often misunderstood or never discussed at all. That gap in planning can quietly cost hundreds of thousands, and in some cases millions, in unnecessary tax.

This isn’t about complex loopholes.

It’s about understanding a powerful opportunity early enough to preserve it.

Why QSBS Matters for Business Owners

When structured correctly, QSBS may allow eligible taxpayers to exclude up to 100% of the gain on the sale of qualifying stock, subject to statutory limits.

This is not a deferral.

This is not a deduction.

This is a true exclusion from tax.

For business owners who are building with a future sale, recapitalization, or liquidity event in mind, QSBS can be one of the most impactful tax outcomes available anywhere in the code.

QSBS Is Won or Lost Long Before an Exit

QSBS is not something you “elect” when a deal is already on the table.

You either qualify or permanently lose the benefit, based on decisions made years earlier.

Eligibility depends on factors such as:

How and when stock is issued

The entity type and underlying business activity

Asset levels at the time of issuance

Required holding periods

How ownership is structured and documented

Miss one requirement, and the exclusion disappears. That’s why QSBS planning must happen before liquidity, not after the paperwork is signed.

Why QSBS Is Getting So Much Attention Right Now

QSBS is resurfacing in planning conversations because:

Business exits are accelerating

More professionals are becoming business owners through acquisitions or startups

Private equity and M&A activity remain strong

High-income earners are actively seeking compliant, high-impact tax strategies

Many business owners are realizing - often after the fact - that they paid tax on gains they didn’t have to.

Where Business Owners Commonly Go Wrong

The most frequent issues I see include:

Assuming their CPA would “bring it up”

Learning about QSBS after the sale

Holding stock personally when trust planning could have multiplied exclusions

Ignoring QSBS eligibility during restructures or entity conversions

QSBS is not a DIY strategy.

It’s not a checklist item.

It’s a design decision that must be made early.

The Strategic Question That Changes Everything

Instead of asking:

“Will this qualify for QSBS?”

The better question is:

“How should this be structured today so QSBS is preserved later?”

That shift, from compliance to forward-looking strategy is where meaningful tax savings happen.

The Bottom Line

QSBS is one of the most generous tax benefits available to business owners and early investors—but only for those who plan early and precisely.

If you’re building, growing, or preparing to exit a business and QSBS has never been part of the conversation, that’s not a coincidence. It’s a signal.

Because once liquidity happens, planning windows close fast.

Next Step

If a future exit - even years away - is part of your long-term plan, understanding whether QSBS applies and how to protect it is a conversation worth having sooner rather than later.

Schedule your call today at

(866) 721-5356

ASK QUESTION

SEND A FILE

SUBSCRIBE

Fill out this form and let us know how we can be of service.

We will offer you a complimentary consultation to determine how we can best serve you.

Ready to Keep More of What You Earn?

Start With Tax Savings Assessment

Discover how much you could be saving with proper tax strategy. Our complimentary assessment typically uncovers $30,000-$50,000 in missed deductions and savings opportunities.

Subscribe to our Mailing List

And that's just a peek at what we offer. Get more marketing tips straight to your inbox.

Contact Us

(866) 721-5356

100 South Bedford Road, Suite 340, Mt. Kisco, New York 10549

© 2024 Chase Eason & Associates, Inc.

100 South Bedford Road, Suite 340, Mt. Kisco, New York 10549